Are you interested to apply for, amend or withdraw a business license?

If any of these apply, use the below button to start the application process online.

If you already applied for a business license and would like to follow the request and get additional information about the process, use our Join Information Portal

Join Information Portal (JIP)Do you want information regarding establishing a business or a certified copy of an already granted license?

Make an appointment

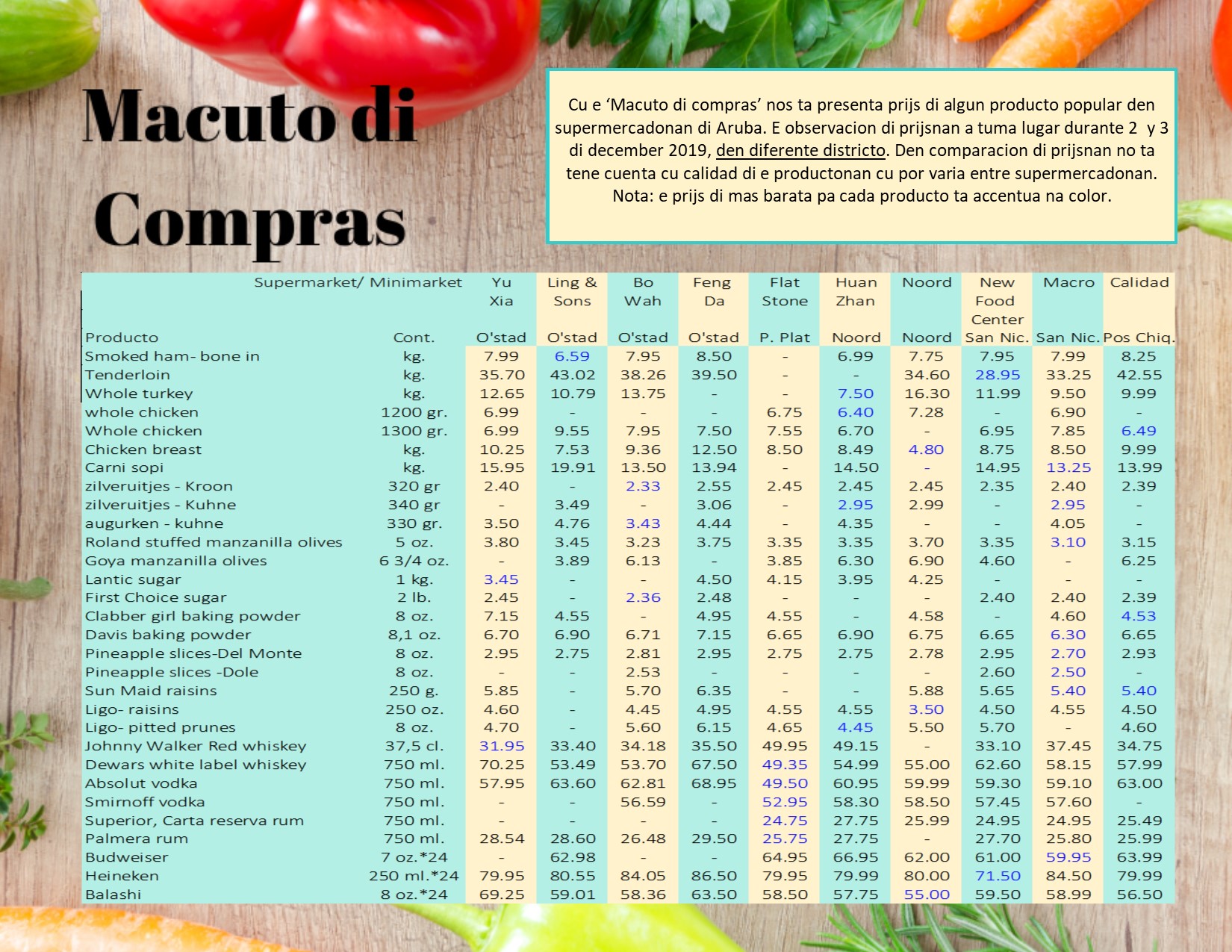

The latest Macuto di Compras published April 16 2024 Regio 1: Oranjestad, Noord, Tanki leendert https://www.deaci.aw/wp-content/uploads/2024/04/15-april-regio-1.png Regio 2: Noord, Oranjestad, Tanki Leendert https://www.deaci.aw/wp-content/uploads/2024/04/15-april-regio-2.png Regio 3: Savaneta, Santa Cruz. Piedra plat, Sanicolas https://www.deaci.aw/wp-content/uploads/2024/04/15-april-regio-3.png […]

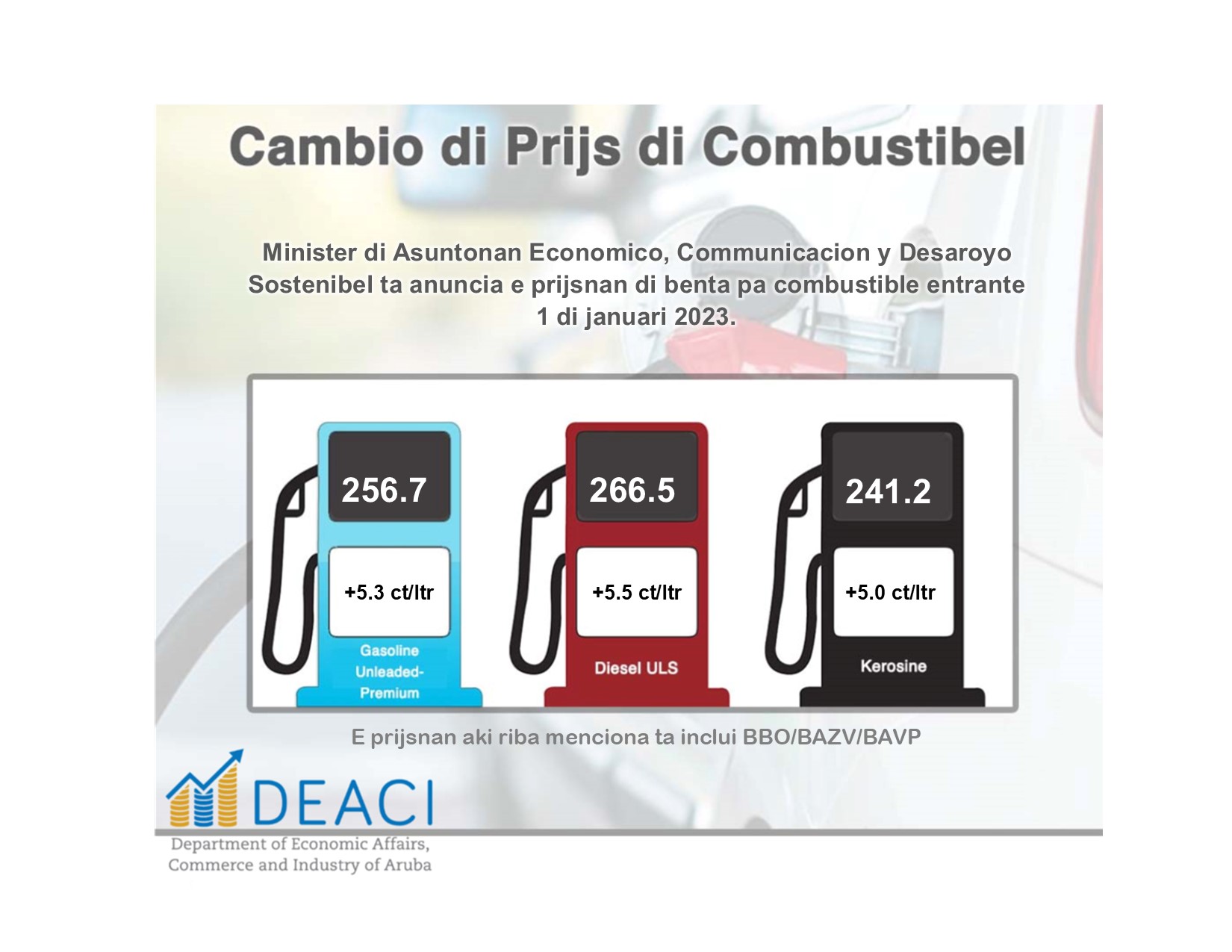

E prijsnan di benta pa combustible, entrante 10 di april 2024, ta bira como lo siguiente: https://www.deaci.aw/wp-content/uploads/2024/04/publicacion-prijs-pa-combustible-10-apr.24.jpg

Contributing to a healthy and sustainable socio-economic development of Aruba by supporting the government in achieving sound economic policies and management.

Department of Economic Affairs,

Commerce and Industry (DEACI)